By Dr. Kalpana | Founder, MoneySavvyUK

As a PhD researcher, I spent years analyzing “efficient systems.” But nothing I studied in the lab was quite as satisfying as finding a legal “glitch” in the UK tax system that lets you keep more of your own money.

That glitch is called Salary Sacrifice.

If you’re a professional mom trying to bridge the gap between your current 9-to-5 and your ultimate “Exit Strategy,” this is the most powerful tool in your kit. However, following the Autumn Budget 2025, the rules are changing. Here is your 2026 blueprint for mastering salary sacrifice.

1. What is Salary Sacrifice? (The “Invisible” Pay Rise)

Salary sacrifice is an agreement between you and your employer to “give up” a portion of your cash salary in exchange for a non-cash benefit—usually a pension contribution.

The Secret Sauce: Because you technically “earn” less, you pay less Income Tax and, crucially, less National Insurance (NI). In 2026, with the standard Personal Allowance still frozen at £12,570, this is one of the few ways to shield your income from “fiscal drag”.

2. The 2026 “Bombshell”: The £2,000 NI Cap

For years, salary sacrifice was the “wild west” of tax savings. But the Chancellor recently confirmed that from April 2029, the NI relief on pension contributions will be capped at £2,000 per year.

What does this mean for you today?

- Current Status (2026): You still get uncapped NI and tax relief. This is the “Golden Window” to front-load your pension before the rules tighten.

- Future Change (2029): You will still get the Income Tax saving on every penny you sacrifice. However, for any amount over £2,000, you and your employer will have to pay National Insurance as if it were normal salary.

The Researcher’s Take: Even after 2029, salary sacrifice remains a “net win” for higher earners because the 40% Income Tax saving is not affected by the cap.

3. Why Salary Sacrifice is a “Mom’s Best Friend”

This isn’t just about retirement; it’s about managing household ROI today. Salary sacrifice lowers your Adjusted Net Income, which is the “magic number” the government uses to calculate your benefits.

- Save Your Child Benefit: The threshold is £60,000. If you earn £63,000, you start losing your benefit. Sacrifice £3,001 into your pension, and you’re back under the limit, keeping 100% of your Child Benefit.

- Keep Your Personal Allowance: If you earn over £100,000, you lose £1 of your tax-free allowance for every £2 you earn. Sacrifice can pull you back under the £100k line, saving you thousands.

- Free Childcare Access: Eligibility for 30 hours of free childcare often cuts off at £100k. Salary sacrifice is the only legal “trapdoor” to stay eligible.

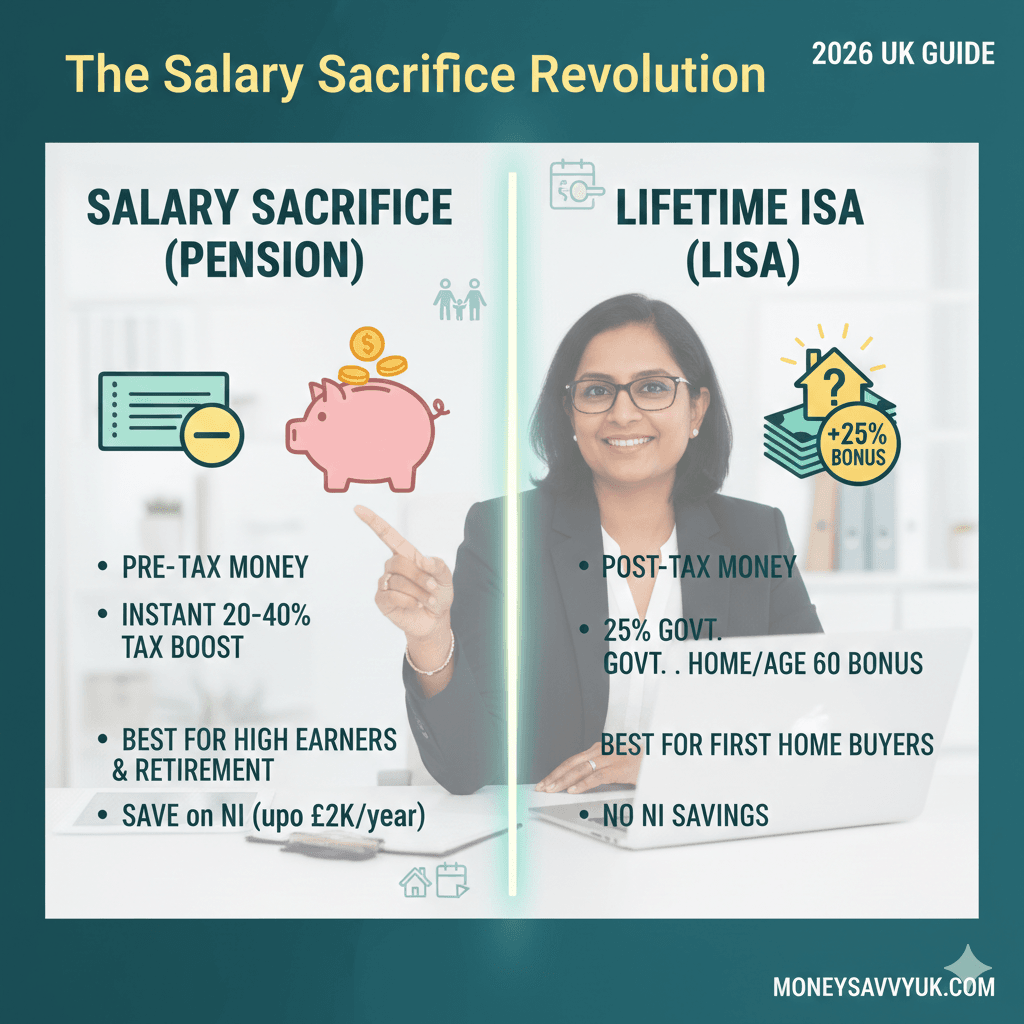

4. Salary Sacrifice vs. The Lifetime ISA (LISA)

Which should you prioritize? I’ve covered this in-depth in my Ultimate Guide to the Lifetime ISA (LISA) in 2026, but here’s the comparison table from the Lab:

| Feature | Salary Sacrifice (Pension) | Lifetime ISA (LISA) |

| Tax Relief | Upfront (20%, 40%, or 45%) | 25% Bonus at the end |

| NI Savings | Yes (until 2029 cap) | No |

| Best For | Higher-rate taxpayers / Retirement | First-home buyers / Under 40s |

| Access | Age 57+ (from 2028) | First home or Age 60 |

Strategy: If you earn over £50,270, use Salary Sacrifice first. The 40% tax saving is better than the 25% LISA bonus. If you are a basic-rate taxpayer saving for a house, use the LISA.

5. The Maternity Pay “Trap”

If you’re planning to grow your family, this is critical. Statutory Maternity Pay (SMP) is calculated based on your average weekly earnings.

Because salary sacrifice lowers your “official” earnings, it can lower your maternity pay.

- The Solution: Many savvy moms “opt-out” of salary sacrifice 2–3 months before their “qualifying week” (usually around week 25 of pregnancy) to ensure their official salary is high. You can then opt back in once you’re back at work.

6. The Top 3 Salary Sacrifice Benefits in 2026

While pensions are the most popular, they aren’t the only game in town:

A. Electric Cars (The EV Loophole)

The “Benefit-in-Kind” (BIK) rates for electric vehicles remain incredibly low through 2026. You can sacrifice salary to lease a new EV, covering insurance and maintenance from your pre-tax income.

B. The Cycle to Work Scheme

Save up to 42% on the cost of a new bike. With the £12.71 National Living Wage rising in April 2026, more workers are eligible for higher-spec bikes through this scheme.

7. Is there a Catch? (The “Researcher’s Warning”)

- Mortgage Multiples: Banks usually look at your “post-sacrifice” salary. If you’re applying for a mortgage soon, a large sacrifice could lower your borrowing limit.

- Life Insurance: If your workplace death-in-service benefit is “4x salary,” check if it’s based on your original or sacrificed salary.

- National Living Wage: You cannot sacrifice so much that your pay drops below £12.71/hr (as of April 2026).

8. FAQs: Your Questions Answered

Can I change my mind?

Under HMRC rules, you can change your sacrifice for “significant life events”—like a new baby or a partner losing a job. Otherwise, your employer may only allow changes once a year.

What happens to my State Pension?

As long as your salary stays above the Lower Earnings Limit (£129/week), you still get a “full year” of NICs towards your State Pension.

Final Verdict: Is it Worth it in 2026?

Absolutely. Even with the upcoming 2029 cap, salary sacrifice is the most powerful way for professional moms to “engineer” their finances and bridge the gap to a 9-to-5 exit.

Are you using salary sacrifice to stay under a tax trap? Let me know in the comments!

Sources & References:

- HM Treasury (2025). Changes to salary sacrifice for pensions from April 2029.

- MoneySavingExpert (Feb 2026). Salary Sacrifice Capped: What it means for you.

- Aviva (2026). Salary Sacrifice Changes: Employee Guide.

- Grant Thornton UK (Dec 2025). Pension salary sacrifice: Changes for employers.