Did you know the average British household spends nearly £1,000 on fun stuff each month1? That’s a lot of money that could help you reach your goals. The 50-30-20 rule is a simple way to manage your money better.

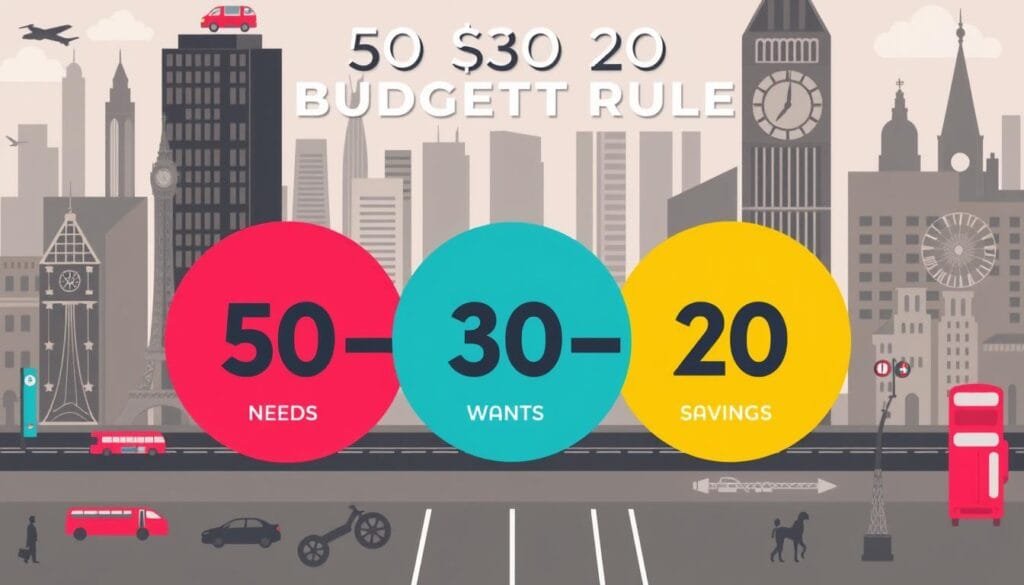

This rule says to split your money into three parts: needs (50%), wants (30%), and savings (20%)1. It helps you see where you spend and find ways to save more. This could lead to financial freedom.

Key Takeaways

- The 50-30-20 rule is a practical budgeting strategy for UK households.

- It divides your income into essential expenses (50%), discretionary spending (30%), and savings/debt repayment (20%).

- This method can help you achieve financial goals and manage your money more effectively.

- The rule can be adjusted to suit individual financial circumstances and priorities.

- Mastering the 50-30-20 approach can lead to greater financial confidence and stability.

Understanding the 50 30 20 Rule UK: A Basic Overview

The 50-30-20 budgeting method is easy to use in the UK. It divides your money into three parts: needs, wants, and savings/debt2. This helps you spend wisely and save for the future.

Origins and Development of the Budgeting Strategy

The 50-30-20 rule started in the United States. It was made to help people manage their money better. Now, it’s popular in the UK too, helping many people with their finances3.

Core Principles of the Rule

The 50-30-20 rule has simple rules:

- 50% of your money goes to basic needs like rent and food.

- 30% is for fun stuff like going out and hobbies.

- 20% is for saving and paying off debts.

Why This Method Works for British Households

The 50-30-20 rule is great for British homes. It’s easy to follow and helps manage money well23. It’s especially useful now, when money is tight.

By using the 50-30-20 rule, families can control their money better. They can make smart choices and save for big goals like a house or retirement23.

Breaking Down the Essential 50% Category

The 50-30-20 rule helps you budget your money. It splits your income into three parts: 50% for needs, 30% for wants, and 20% for savings4. If you earn £27,904 a year, you’d spend £1,162.50 on needs4.

What are your essential needs? These include rent, bills, food, and transport5. In the UK, the average mortgage payment is £747. This leaves £415.50 for other needs4.

Food costs £136 a month, and bills are £66.03 and £61.54 for gas and electricity4. This leaves £151 for things like phone and internet4.

Planning your 50% needs helps you meet your basic needs first4. This way, you can save and spend wisely4.

The 50-30-20 rule is easy to follow. It helps you focus on needs while still saving and spending5. It’s a good way to manage your money and secure your future5.

But remember, this is just a guide. You might need to change it based on your own money situation5. The important thing is to stay flexible and adjust as needed5.

“Planning and budgeting towards savings goals using the 50-30-20 rule can help individuals stay mindful of their finances and make positive changes to their spending habits.”

Allocating 30% to Lifestyle and Wants

The 50/30/20 rule says to use 30% of your money for fun and wants7. This includes things like eating out, going to shows, and buying new clothes. It’s a way to enjoy life while still saving and paying bills.

Discretionary Spending Examples

Here are some things you can spend 30% on:

- Dining at restaurants and cafés

- Subscriptions to streaming services, magazines, or gym memberships

- Hobbies and recreational activities, like sports, concerts, or travel

- Clothing, electronics, and other non-essential purchases

Spending on these things helps you balance saving and having fun7.

Managing Entertainment and Leisure Costs

Entertainment and fun can take up a lot of your budget. Choose activities that make you happy. This way, you spend money on things that matter to you. It helps you enjoy your life and stay balanced7.

Balancing Lifestyle Choices

Finding the right mix of needs, wants, and savings is crucial. The 30% for wants gives you room for fun. But, make sure it doesn’t hurt your money future7. Check your spending often and adjust to keep your finances healthy.

“The 50/30/20 rule is a simple and effective way to manage your finances, allowing you to enjoy life’s pleasures while still prioritising your financial security.”

Using the 50/30/20 rule helps you manage your money well. It supports your lifestyle and future plans7. It’s a good way to save for big things, pay off debt, or just have more money.

Maximising the 20% Savings Portion

The 20% savings part is key in the 50/30/20 rule. It helps you stay financially stable8. This money goes into an emergency fund, for future investments, and to pay off debts. All these steps help your financial health.

To use this 20% wisely, think about automating your savings9. Set up automatic transfers to a savings account. This way, the money is saved before you can spend it. Also, use apps like Mint9 to track your spending and find ways to save more.

The 50/30/20 rule is just a guide. You can change the percentages based on your needs10. If you have a lot of debt, you might save less to pay it off faster10. But if you spend less on basics, you can save more for the future.

| Budgeting Category | Percentage | Example (£2,000 Monthly Income) |

|---|---|---|

| Needs | 50% | £1,000 |

| Wants | 30% | £600 |

| Savings/Debt | 20% | £400 |

By sticking to the 50/30/20 rule and focusing on savings, you can reach your financial goals10. It’s important to stay flexible and adjust your spending and saving as needed. This way, you can always meet your changing financial needs.

“The 50/30/20 rule is a simple yet powerful framework that can help you take control of your finances and achieve financial stability. By dedicating a substantial portion of your income to savings, you’re setting yourself up for long-term success.”

Practical Application in British Households

The 50-30-20 budgeting rule helps manage money well. It works for different incomes in the UK. Using the UK national average wage of £33,000, it splits money into needs, wants, and savings. This is about £1,100 for needs, £660 for wants, and £440 for savings or debt each month11.

Adjusting the Rule for Diverse Income Levels

While the 50-30-20 rule is a good start, you can change it to fit your needs. If you earn less, you might need to adjust the percentages. This could mean a 70-20-10 or a budget just for you12.

If you earn more, you might save more. You could aim for a 40-30-30 or 40-20-40 split. The goal is to match your spending with your goals13.

Keep track of your spending and see if it fits the 50-30-20 rule. If not, you can change it. This helps you save for big things like a house or to pay off debts13.

“The 50-30-20 rule is a simple yet effective way to take control of your finances and build a solid financial foundation. By allocating your income appropriately, you can ensure your essential needs are met, your lifestyle is balanced, and your savings are prioritised.”

How well a budget works depends on your income, costs, and goals. Try different budgets to find what’s best for your home in Britain12.

Common Challenges and Solutions

Using the 50-30-20 budgeting rule in the UK can be tricky. But, it can still work well for many families14. Unexpected costs like medical bills or car repairs can mess up the plan14. Also, people with changing incomes or living in different parts of the UK might find it hard to stick to the rule14.

To beat these problems, setting up an emergency fund helps. It lets you adjust the budget to fit your life better14. It’s also key to keep checking and tweaking your budget. This way, the 50-30-20 rule stays useful, even when money is tight14.

| Income Level | Needs (50%) | Wants (30%) | Savings (20%) |

|---|---|---|---|

| £34,000 annually | £1,166 | £700 | £467 |

| £60,000 annually | £1,890 | £1,134 | £756 |

The table shows how the 50-30-20 rule works for different incomes15. For some, a 65-15-20 split might be better15. The goal is to find a budget that fits your goals and lifestyle15.

Knowing the challenges and being flexible with the 50-30-20 rule can help you reach your money goals. The 50/30/20 rule may not work for everyone. But, with a flexible mindset, it can be a great tool for managing money1415.

Tools and Resources for Budget Management

Using the 50-30-20 rule for budgeting is easier with digital tools. Online budget calculators help you sort your money. They put your income and expenses into three groups: needs, wants, and savings16.

These tools show you how you spend money. They help you see where to change your budget16.

Digital Apps and Calculators

Many apps in mobile banking help track your spending. They let you sort your money into categories16. These apps connect to your bank accounts and cards. They give you updates on your money in real time5.

Spreadsheet Templates and Planners

Spreadsheet templates and planners are great for hands-on budgeting. You can put in your income and expenses yourself. Then, they show how much you should save and spend16.

They are good for those who like to control their budget. Or if you need a budget plan that fits you5.

| Tool | Key Features | Advantages |

|---|---|---|

| 50/30/20 Rule Calculator | Automatically allocates income based on the 50-30-20 rule | Provides a clear visual breakdown of spending categories |

| Budget Planner Spreadsheet | Allows manual input of income and expenses, with automated calculations | Offers greater control and customisation for individual budgeting needs |

| Mobile Budget Tracking Apps | Syncs with bank accounts and credit cards to categorise expenses | Provides real-time insights and updates on spending habits |

Using these tools makes budgeting easy. They help you stick to the 50-30-20 rule and reach your money goals165.

“Budgeting can be a daunting task, but with the right tools, it becomes much more manageable. The 50-30-20 rule provides a straightforward framework, and these digital resources make it easy to put it into practice.”

There are many tools to help you manage your money. You can choose apps or spreadsheets. They all help you reach your financial goals165.

Adapting the Rule for Different Life Stages

The 40-30-20-10 rule is great for all life stages. It helps you manage money well, no matter if you’re a student, young worker, family, or retiree17.

Students might spend more on school, home, and basic needs18. As they earn more, they can save more for the future18.

Families might spend more on kids’ needs like school and health19. Retirees should save more and spend on health and fun.

It’s important to be flexible with the rule18. Regularly check your budget and adjust as needed. This way, the 40-30-20-10 rule helps you reach your financial goals at any stage17.

| Life Stage | Needs (%) | Wants (%) | Savings (%) | Miscellaneous (%) |

|---|---|---|---|---|

| Students | 60 | 25 | 15 | 0 |

| Young Professionals | 40 | 30 | 20 | 10 |

| Families | 45 | 25 | 20 | 10 |

| Retirees | 50 | 20 | 25 | 5 |

The 40-30-20-10 rule is a good start, but it might not always be the best18. Adjusting it to fit your financial goals helps you stay financially stable and successful.

“The 40-30-20-10 rule is a great starting point, but it’s crucial to be adaptable and make adjustments as your life circumstances change. The key is to find a budgeting strategy that truly works for you.”

By making the 40-30-20-10 rule your own, you can manage your money well at any stage191718.

Impact of Cost of Living Crisis on Budgeting

The cost of living crisis in the UK is making budgeting hard for many20. Rent, council tax, and utility bills are very expensive. Sometimes, rent alone takes up to 25% of what people earn20.

This makes it tough to stick to the 50/30/20 budgeting rule. The rule says to spend 50% on needs, 30% on wants, and 20% on savings20.

Regional Variations Across the UK

The cost of living crisis hits different parts of the UK in different ways. The South East and London face higher costs for housing and transport21. This means households in these areas might need to change their budgeting plans.

Inflation Considerations

High inflation is also affecting budgets22. As prices go up, the ‘needs’ part of the 50/30/20 rule might need to grow. This could leave less for wants and savings22.

It’s important to regularly check and adjust budgets. This helps the 50/30/20 rule work even when money is tight212220.

In summary, the cost of living crisis in the UK is making budgeting harder. With regional differences and high inflation, households need to watch their spending closely. They might need to adjust the 50/30/20 rule to fit their financial situation212220.

“The 50/30/20 rule is a useful guideline, but the current economic climate may require some households to be more flexible in their budgeting approach.”

Alternative Budgeting Methods vs 50/30/20

The 50/30/20 budgeting rule is popular but not for everyone23. Only 17% of UK consumers say it works for them23. People are now looking for other ways to manage their money.

Zero-based budgeting is one method. It means every pound is spent on something specific24. This way, you think about each purchase carefully. The envelope system is another. It uses cash in different envelopes for different things, helping you stick to your budget.

23 Many people use different ratios like 60-30-10 or 70-20-1023. Some find the 60-30-10 ratio works for them23. Others prefer the 70-20-10 method23.

23 Some use an 80-10-10 or 90-10-0 ratio23. Others stick to 80-20-0 or 70-30-023.

23 A few use a 90-5-5 or 60-40-0 ratio23. Some even spend more than 100% on essentials, leading to debt23.

Finding the right budgeting method is key. It should help you save, spend wisely, and reach your financial goals. Whether it’s 50/30/20, zero-based, or something else, the right plan can lead to financial freedom.

Tips for Long-term Success with the Strategy

To succeed with the 50 30 20 rule uk, you need to keep trying and check your progress often. Keep track of how you’re doing, noting any changes from the set percentages25. Be ready to change the rule if your life or money needs change25.

Setting up automatic savings can help you stick to your saving money goals. This makes saving easier and more regular.

It’s also important to check your money goals often. If your needs are less than 50%, you might save more, like 40/30/30 or 30/40/3026. If 20% isn’t enough for you, you could try a 70/20/10 split26.

Even small changes can help a lot over time. They can make your money situation better and more stable. By being flexible with the 50 30 20 rule uk and keeping an eye on your budget, you’re on the path to financial success.

FAQ

What is the 50-30-20 rule in the UK?

The 50-30-20 rule helps people in the UK manage their money. It says to spend 50% on things you need, 30% on things you want, and 20% on saving or paying off debt.

How does the 50-30-20 rule work in practice for British households?

It divides spending into three parts. 50% goes to needs like rent, bills, and food. 30% is for wants like eating out and shopping. The last 20% is for saving or paying off debt.

What are the benefits of using the 50-30-20 rule for budgeting in the UK?

It helps people in the UK focus on spending and save money. It’s easy to adjust for different incomes and financial situations. This makes it a great tool for financial stability.

How can UK residents implement the 50-30-20 rule effectively?

To use it well, track your spending and sort it into needs, wants, and savings. Use digital tools and budget calculators to help. This makes managing money easier.

What are some common challenges in applying the 50-30-20 rule in the UK?

Unexpected costs and changing income can be tough. Also, costs vary by region. To overcome these, have an emergency fund and adjust your budget as needed.

How can the 50-30-20 rule be adapted for different life stages in the UK?

It can be changed for different life stages. For example, students might save more for the future. Young families might spend more on needs. Adjust the percentages to fit your life.

How has the UK cost of living crisis impacted the use of the 50-30-20 rule?

The crisis has made budgeting harder. You might need to spend more on needs due to rising costs. Adjust your budget to fit your local costs and inflation.

Are there any alternative budgeting methods to consider besides the 50-30-20 rule in the UK?

Yes, there are other ways to budget like zero-based budgeting or the envelope system. Try different methods to find what works best for you and your money goals.

Source Links

- How much of my salary should I save? | 50-30-20 rule – YBS – YBS DXP Prod – https://www.ybs.co.uk/savings/guides/50-30-20-rule

- What’s the 50 30 20 budget rule? – https://www.equifax.co.uk/resources/money-management/50-30-20-budget-rule.html

- The 50/30/20 rule | What is the 50/30/20 budgeting rule? – https://www.co-operativebank.co.uk/tools-and-guides/50-30-20-rule/

- Debt To Deposit: The 50-30-20 Savings Model – https://moneyplusadvice.com/blog/tips-advice/how-using-the-50-30-20-model-can-help-you-save/

- The 50/30/20 Budgeting Rule — Moneyhub – https://www.moneyhub.com/blog/2024/3/18/the-503020-budgeting-rule

- Budgeting Methods: 50/30/20 Rule | Atom bank – https://www.atombank.co.uk/blog/budgeting-50-20-30-rule/

- The 50/30/20 Rule: A Complete Guide to Managing Your Money More Efficiently – https://www.femaleinvest.com/en-gb/magazine/the-50-30-20-rule-a-complete-guide

- What Is The 50/30/20 Rule? – https://www.forbes.com/advisor/banking/guide-to-50-30-20-budget/

- How to budget and save money – https://www.saga.co.uk/savings/how-to-budget-and-save-money?srsltid=AfmBOoo-x8o-h4RO8eOvgx5WaMTstZO1TFiL5dco4M0oBSlohmZkiDJg

- 50/30/20 Rule: Budgeting Tips And Money-Saving Advice – https://foundered.co.uk/50-30-20-rule/

- Budget rules: what are they and which is best for you? – https://www.onefamily.com/savings/budget-rules-what-are-they-and-which-is-best-for-you/

- 50/30/20 rule: Is it realistic in a cost of living crisis? – Starling Bank – https://www.starlingbank.com/blog/50-30-20-budgeting-rule-is-it-realistic-in-a-cost-of-living-crisis/

- What is the 50 30 20 rule? – https://www.raisin.co.uk/savings/what-is-the-50-30-20-rule/

- How the 50-30-20 budgeting ‘rule of thumb’ is changing – https://www.pensionbee.com/uk/blog/2022/october/how-budgeting-rules-are-changing-in-cost-of-living-crisis

- How the 50/30/20 budgeting hack can unlock your finances – https://www.telegraph.co.uk/money/banking/current-accounts/what-503020-budgeting-method/

- How to calculate your monthly savings potential with the 50/30/20 budget – Metfriendly – https://www.metfriendly.org.uk/how-to-calculate-your-monthly-savings-potential-with-the-50-20-30-budget/

- Budgeting Made Easy: A Guide to the 50/30/20 Rule – https://www.johnnydebt.co.uk/money/budgeting-made-easy-a-guide-to-the-50-30-20-rule/

- The 50/30/20 budget rule: what are the pros and cons? – https://www.fool.co.uk/2021/07/15/the-50-30-20-rule-what-are-the-pros-and-cons/

- 50/30/20 Rule: A Beginner’s Guide on How to Conquer Your Finances – https://www.equentis.com/blog/50-30-20-rule/

- ‘I found out if the 50/30/20 budget is realistic during a cost of living crisis’ – https://www.manchestereveningnews.co.uk/news/cost-of-living/i-tried-503020-budget-see-26477687

- How to budget during a cost of living crisis – https://www.equifax.co.uk/resources/money-management/budget-during-cost-of-living

- Money Management: How to Budget | Marsden Building Society – https://www.themarsden.co.uk/support-and-guidance/money-management-how-to-budget

- The 70-20-10 money rule: the new and better way to save – https://hyperjar.com/blog/the-70-20-10-rule

- Making A Budget & Managing Money – My Debt Plan – https://mydebt-plan.co.uk/budgeting/

- The 50/30/20 rule: the ‘easy’ budgeting hack explained – https://theweek.com/business/personal-finance/958947/the-503020-rule-the-easy-budgeting-trick-explained

- 5 Ways To Alter the 50/30/20 Rule To Suit Your Savings Plan – https://uk.finance.yahoo.com/news/5-ways-alter-50-30-180042865.html